Two percent. In countless German auto repair shops, this small number determines whether an invoice is legally sound or whether the customer will successfully challenge it. Anyone who wants to correctly calculate the small-parts surcharge in CATAMA must understand why this seemingly trivial flat fee has been a topic of debate among courts, experts, and insurers for years. And why a transparently reported percentage ultimately secures more revenue than any flat-rate estimate.

This guide is intended for auto shop owners, service managers, and bookkeepers in the automotive industry who want to structure their small-parts flat fee in a legally compliant manner, justify it soundly from a business perspective, and enter it correctly into their shop management software. No legal jargon—just clear recommendations for action.

Key Takeaways

- Two percent of the value of the replacement part or repair is considered the legally established upper limit for flat-rate billing without itemized documentation.

- The small-parts surcharge must be clearly itemized on the invoice; hidden surcharges are open to challenge.

- Avoid double billing: Items that have already been billed separately (such as larger gaskets) must not be included in the flat rate again.

- Higher rates (3, 4, or 5 percent) are possible, but require a reliable calculation of actual consumption based on your own data.

- Accurate recording in the workshop software ensures consistent, audit-ready invoices and protects against reductions by insurers.

What exactly is the small-parts surcharge?

The small-parts surcharge, also known as the small-parts flat fee or small-parts supplement, is a flat-rate charge for consumables that are used in every repair but cannot be economically tracked on an individual basis. These include:

- Screws, nuts, washers, cotter pins

- Cable ties, clamps, electrical tape

- Cleaning agents, brake cleaner, contact spray

- Small amounts of sealant, grease, copper paste

- Cleaning cloths, gloves, plastic sheeting

- Locks, small clips, holders

Tracking these materials individually would make no business sense. The time required to record a 2-cent clip far exceeds its value. This is precisely why flat-rate billing has been the standard in the automotive industry for decades, and the courts have generally recognized this practice.

Why have a flat rate at all?

Without a flat fee for small parts, the repair shop is left to cover the costs. If you include a single 15-cent cable tie on an invoice, it seems petty. If you don’t include it, you lose margin. With thousands of repairs a year, these small amounts add up to four- to five-digit losses in revenue.

Key point: The small-parts flat rate is not a profit margin on small parts, but rather the only economically sensible method for accounting for consumables in the cent range.

The 2-Percent Rule: What the Courts Actually Say

The oft-cited “2 percent of the value of the replacement part or repair” is not a figure set by law, but has established itself over the years in case law as a guideline. Various local and regional courts have recognized this figure as reasonable and recoverable without the need for individual proof, particularly in the context of liability claims and settlements with opposing insurers.

The Key Points of the Case Law

First: A markup of about 2 percent on the cost of replacement parts (and in some cases on the total repair cost, including labor) is considered standard practice in the industry and reasonable. Insurance companies generally cannot simply reduce this amount.

Second: The flat fee must be clearly itemized on the invoice. A hidden surcharge included in the hourly rates or added to the prices of replacement parts is open to challenge.

Third: There must be no double billing. If a small part (e.g., a specific sealing ring) is already listed as a separate item on the invoice, it must not be included in the basis for calculating the flat fee.

Fourth: Higher flat rates (3, 4, 5 percent, or more) are not per se impermissible. The higher the markup, the greater the repair shop’s obligation to justify it—ideally through its own documented calculation.

Basis for Assessment: Replacement Parts or Total Value?

There are two common models here:

| Model | Tax Base | Practice |

|---|---|---|

| Narrow interpretation | Net value of replacement parts only | Conservative, less likely to cause conflict |

| Broad interpretation | Replacement Parts + Labor Costs | Higher amounts are more often reduced by insurers |

The prevailing case law tends toward a narrow interpretation, i.e., 2 percent of the value of the replacement part alone. Anyone who includes labor costs in the calculation basis should be able to agree to this with the customer in the contract and justify the decision.

Calculating the Small Parts Surcharge Correctly in CATAMA: Your Own Cost Estimate

Anyone who doesn't want to settle for the blanket 2-percent solution should determine the actual small-parts consumption in their own business. This is particularly worthwhile for specialized repair shops (e.g., bodywork, electrical systems, classic cars), where actual consumption is significantly higher than average.

Step-by-Step Guide to Doing Your Own Cost Estimate

1. Define the data collection period

Select a representative time period, ideally 3 to 6 months. Shorter periods can lead to distortions caused by one-time events.

2. Isolate Purchases of Small Parts

Tally all purchases of consumables that are not billed on a per-order basis. These include screw assortments, cable tie boxes, cleaning supply containers, gloves, cleaning cloths, etc. A structured inventory management system makes this analysis much easier.

3. Determine the tax base

Determine the total sales of replacement parts (or, depending on the model: replacement parts + labor) for the same period.

4. Calculate the percentage

Prozentsatz = (Kleinteileverbrauch / Ersatzteilumsatz) × 100

Sample calculation:

- Purchases of small parts over 6 months: 4,800 euros net

- Spare Parts Sales for 6 Months: 165,000 euros net

- Percentage: (4,800 / 165,000) × 100 = 2.91 percent

In this example, a flat rate of approximately 2.9 percent would be justifiable from a business perspective and could be documented in the event of a dispute.

5. Retain Documentation

Retain the cost estimate, the supporting documents, and the basis for calculation for at least 10 years. This will allow you to provide complete documentation of how your markup was calculated whenever requested by insurers, customers, or the tax authorities.

Set Upper and Lower Limits Appropriately

Many repair shops operate with an absolute upper limit, such as a maximum of 25 or 50 euros per job. For an engine overhaul with 12,000 euros worth of replacement parts, 2 percent would amount to 240 euros—an unrealistically high amount for screws and cable ties. Setting a cap gives the impression of professionalism and prevents disputes.

Another sensible idea: a minimum flat fee of about 3 to 5 euros for very small orders, so that the administrative effort is worth it.

Practical Implementation: Calculating the Small Parts Surcharge Correctly in CATAMA

Good repair shop software completely eliminates the need for manual cost calculations. In modern cloud-based solutions for auto repair shops, the small-parts surcharge is stored in the system as a configurable item and is automatically calculated correctly for every job.

What a Professional Configuration Includes

- Define the percentage centrally (e.g., 2%); can be changed with a single click

- Select the basis for calculation: spare parts only, or including labor

- Maintain Exclusion Lists: Certain product groups (tires, batteries, large assemblies) are excluded from the tax base

- Define maximum and minimum limits

- Automatically listed as a separate line item on the invoice with a clear description

- Assign the correct tax treatment (standard tax rate of 19%)

The advantages are obvious: No employee has to calculate the flat rate manually anymore, there are no typos, and every invoice is consistent and audit-proof. Anyone who takes a closer look at the benefits of industry-specific software for auto repair shops will quickly realize just how much administrative work is eliminated by such automated processes alone.

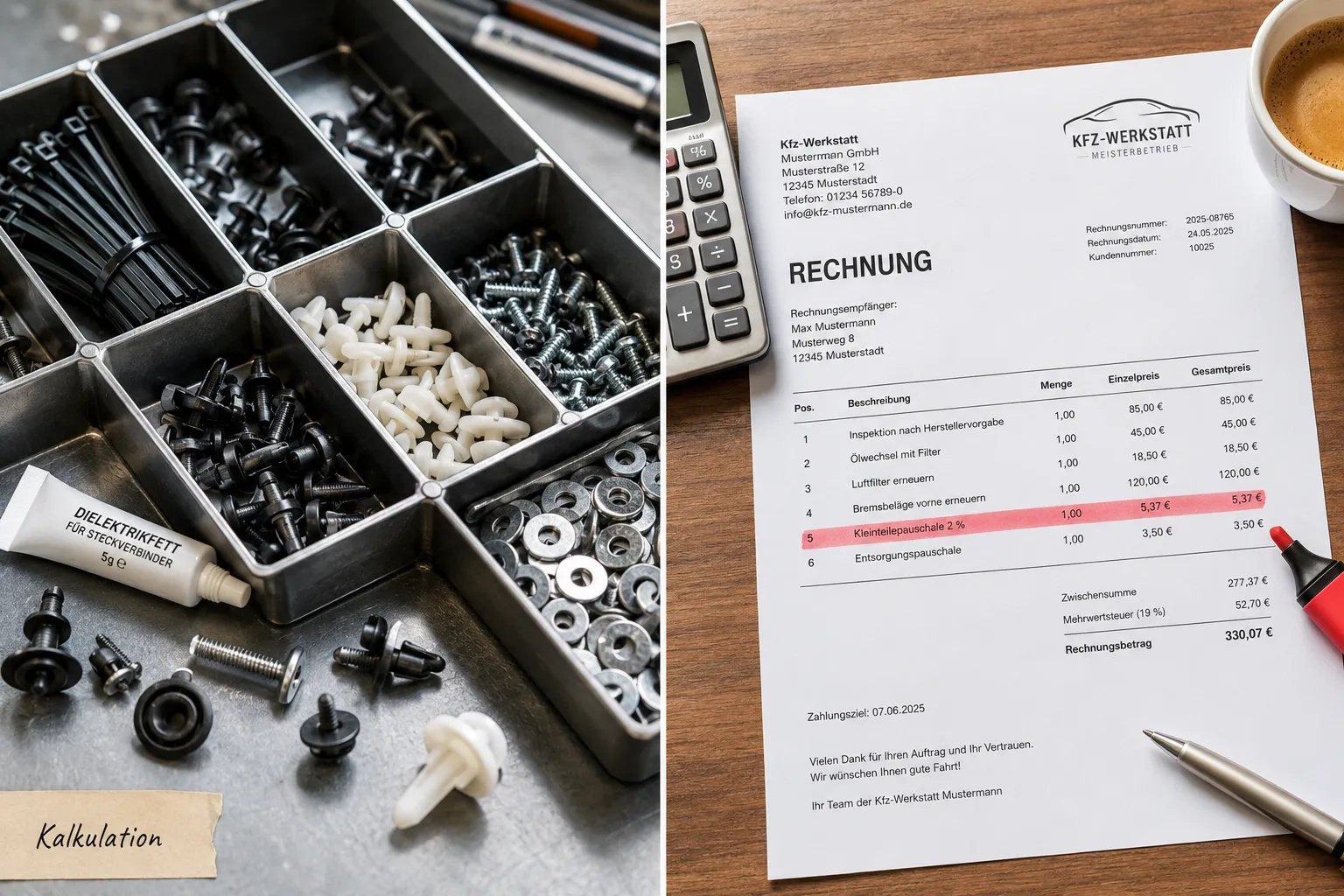

Sample wording for the invoice

The transparent disclosure should be clearly and legally soundly worded. Terms such as the following have proven effective:

- "Small Parts Fee (2% on replacement parts)"

- "Flat-rate 2% surcharge for small items"

- "Consumables (flat rate as per price list)"

Avoid vague terms such as “Other” or “Incidental expenses”; such phrasing is a common reason for reductions.

Common Mistakes and How to Avoid Them

Error 1: Double billing for small parts

Problem: A specific gasket is listed separately on the invoice at 8.50 euros, yet this amount is still included in the calculation basis for the 2 percent flat rate.

Solution: In the inventory management system, exclude all small items that are billed individually from the calculation basis for the flat rate. Good software allows you to explicitly mark item groups.

Error 2: Lack of Transparency in Reporting

Problem: The markup is hidden in the spare part price or appears only as a collective line item labeled “Incidental Costs.”

Solution: Always include a separate, clearly labeled invoice line item with the percentage and the tax base.

Error 3: Excessive flat fee without justification

Problem: The repair shop applies a flat rate of 5 percent without being able to substantiate this figure with calculations.

Solution: Either revert to the standard 2 percent or document your own calculation.

Error 4: Assessment Basis Defined Incorrectly

Problem: Tires, batteries, and replacement units are included in the calculation basis, even though these items do not involve any significant consumption of small parts.

Solution: Define an exclusion list for high-volume items. Rule of thumb: Items exceeding a certain unit value (e.g., 200 euros) or belonging to certain product categories are not included.

Mistake 5: No cap

Problem: Very major repairs (engine failure, transmission failure) result in absurdly high flat fees in the three- or four-digit range.

Solution: Set a reasonable upper limit and document it in the price list.

Calculating the Small Parts Surcharge Correctly in CATAMA and Distinguishing It from the Used Parts Tax

A common misconception: The small-parts allowance and the used-parts tax are two completely different matters. While the small-parts allowance covers the use of new small parts, the used-parts tax concerns the VAT treatment of returned used parts (such as replacement engines).

Both items may appear on the same invoice, but they must be strictly separated for accounting and tax purposes. Anyone who is unsure about this should review the guidelines for correctly reporting the tax on severance pay; a clear separation protects against additional tax assessments from the tax office.

Communication with Customers and Insurers

Dealing with Individual Customers

Most residential customers will accept a transparently stated 2 percent flat fee without asking questions. It’s important to communicate this clearly in advance, for example in the estimate or in the repair shop’s terms and conditions. If you wait until the invoice to “reveal” the flat fee, you’ll cause unnecessary frustration.

Dealing with Insurance Companies

In cases of liability and comprehensive insurance claims, insurers regularly attempt to reduce or completely eliminate the small-parts allowance. Arguments to support your case:

- Based on relevant case law, 2 percent is considered standard for the industry and reasonable.

- Reference to the repair shop price list, which the customer was aware of before placing the order.

- Submit your own calculation as proof if the rates are higher.

- Consistent, accurate invoicing and a professionally designed automotive invoicing program significantly reduce the risk of payment reductions.

Dealing with Commercial Customers and Fleets

For framework agreements with fleet customers, car rental companies, or leasing companies, flat rates for small parts should be explicitly agreed upon. Reduced rates (e.g., 1.5%) or fixed amounts per order are often negotiated in these cases. Important: The agreed-upon terms must be entered into the system and applied automatically; manual exceptions are prone to errors.

Interaction with Hourly Rates and Material Surcharges

The small-parts surcharge is just one of several factors in workshop cost calculations. It works in conjunction with:

- The hourly billing rate (see hourly rate calculator for auto repair shops)

- The markup on replacement parts (typically 20–40% of the purchase price)

- Revenue per order and contribution margin analysis

- Additional services such as car cleaning, pick-up and drop-off service

Anyone who calculates all the individual components separately and transparently has a clear advantage over competitors who use flat rates: During discussions with clients or insurers, individual items can be justified precisely; nothing looks less professional than an opaque lump-sum invoice.

Digitization as a Prerequisite for Accurate Cost Estimation

Without digital shop software, it’s nearly impossible to implement a consistent, audit-proof flat rate for small parts. There are too many manual steps and too many sources of error. With a modern shop management system, the following processes run automatically:

- Calculating the Correct Tax Base for Each Order

- Application of Percentages and Caps

- Exclusion of Specific Product Categories

- Reported as a separate line item on the invoice

- VAT Accounting

- Analysis of Actual vs. Calculated Small Parts Consumption

This last point, in particular, is crucial: Only by regularly checking whether the calculated flat rate actually covers actual consumption can you ensure the long-term viability of your pricing structure and contribution margin.

Practical Checklist: 7 Steps to a Proper Small Parts Flat Rate

- Set a percentage—2% as a safe default, or use your own calculation for higher rates

- Define the basis for calculation: spare parts only, or including labor

- Create an exclusion list; exclude tires, batteries, and large assemblies

- Set a cap, e.g., a maximum of 50 euros per order

- Configure the software, enter a flat rate centrally, and apply it automatically

- Update the price list and terms and conditions, and document them transparently for customers

- Check regularly; perform an annual comparison between actual consumption and the calculated flat rate

Conclusion: Transparency trumps discussion

The small-parts surcharge is not a legal gray area, but rather a position on every repair shop invoice that has been upheld by the courts for years. Anyone who sticks to the tried-and-true 2 percent, lists it transparently as a separate line item on the invoice, and avoids double billing is on the safe side—with customers, insurers, and, if necessary, in court.

If you want to charge higher rates, you need a solid cost analysis of your own. The effort involved is manageable and is well worth it for specialized businesses.

Next steps:

- Check your recent bills: How is the small-item fee currently listed? Is it transparent or hidden?

- Track your own usage: Compare three months of small-parts purchases to spare-parts sales, and you'll know your actual ratio.

- Check your software: Can your system calculate the flat rate automatically, in a configurable manner, and based on exclusions? If not, a free trial of a modern workshop solution is a sensible next step.

- Update the price list and terms and conditions: Clear communication prevents disputes later on.

- Train the team: Service staff and the accounting department need to know when the flat rate applies and when it does not.

A clear, audit-proof flat rate for small parts isn’t just a minor detail for the accounting department—it’s a direct contributor to your shop’s bottom line. Two percent may seem insignificant, but over the course of a year, it’s often the difference between a loss and breaking even.